Treasury QuestionnaireApril

Treasury QuestionnaireApril

《Treasury QuestionnaireApril》由会员分享,可在线阅读,更多相关《Treasury QuestionnaireApril(4页珍藏版)》请在装配图网上搜索。

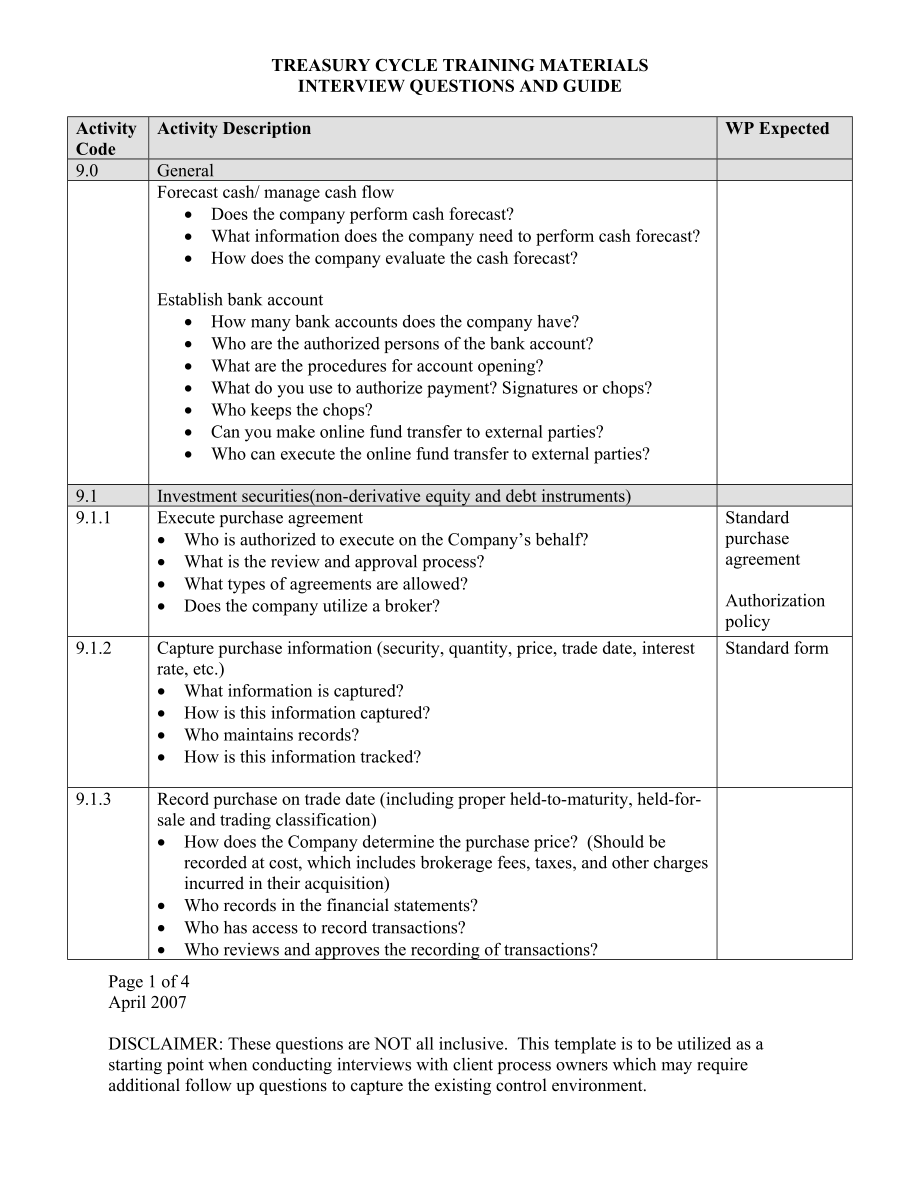

1、TREASURY CYCLE TRAINING MATERIALSINTERVIEW QUESTIONS AND GUIDEActivity CodeActivity DescriptionWP Expected9.0GeneralForecast cash/ manage cash flow Does the company perform cash forecast? What information does the company need to perform cash forecast? How does the company evaluate the cash forecast

2、?Establish bank account How many bank accounts does the company have? Who are the authorized persons of the bank account? What are the procedures for account opening? What do you use to authorize payment? Signatures or chops? Who keeps the chops? Can you make online fund transfer to external parties

3、? Who can execute the online fund transfer to external parties?9.1Investment securities(non-derivative equity and debt instruments)9.1.1Execute purchase agreement Who is authorized to execute on the Companys behalf? What is the review and approval process? What types of agreements are allowed? Does

4、the company utilize a broker?Standard purchase agreementAuthorization policy9.1.2Capture purchase information (security, quantity, price, trade date, interest rate, etc.) What information is captured? How is this information captured? Who maintains records? How is this information tracked?Standard f

5、orm9.1.3Record purchase on trade date (including proper held-to-maturity, held-for-sale and trading classification) How does the Company determine the purchase price? (Should be recorded at cost, which includes brokerage fees, taxes, and other charges incurred in their acquisition) Who records in th

6、e financial statements? Who has access to record transactions? Who reviews and approves the recording of transactions?9.1.4Calculate and record accruals and receipts of interest Who is responsible for recording accruals? What types of accruals do you have? What types of assumptions are used in the c

7、alculations? How often are the calculations reviewed for reasonableness? What is the review and approval process? How often do you receive interest payments? How is interest recorded in the system? Who records interest payment in the system?9.1.5Calculate and record amortization of premiums and accr

8、etion of discounts Do you have an amortization schedule? How often is the schedule reviewed and updated? Who reviews and approves?Amortization schedule9.1.6Calculate and record changes in carrying value of investment securities How does the Company ensure compliance with FASB Statement No. 115? (Thi

9、s statement was issued to address the valuation of securities. The statement applies to all debt securities and to equity securities for which a readily determinable fair value is available.) Who is responsible for the accurate classification of securities? (trading, held-to-maturity and available-f

10、or-sale) Does the Company have a policy in place regarding the transferring of debt securities between categories?o Who approves?o How is the carrying value calculated? o How do you ensure compliance with FAS Statement No. 115?o Who reviews and approves the calculations?o Who reviews the carrying va

11、lue for reasonableness?9.2Derivative contracts (non-inventory-related)9.2.1Execute contract Who is authorized to execute on the Companys behalf? What is the review and approval process? What types of agreements are allowed? Does the company utilize a broker?9.2.2Complete hedge documentation (if appl

12、icable) What information is captured? How is this information captured? Who maintains records? How is this information tracked?9.2.3Record related assets and liabilities Who has access to record? Who reviews? How is activity tracked? What reconciliations are performed?9.2.4Calculate and record perio

13、dic market valuation adjustments in accordance with applicable accounting standards Who has access to record? Who reviews?9.2.5Calculate and record settlements for related contracts Who has access to record? Who reviews? How is activity tracked? What reconciliations are performed?9.3Other unique/com

14、plex transactions (e.g. securitizations, etc.)9.3.1Execute contract Who is authorized to execute on the Companys behalf? What is the review and approval process? What types of agreements are allowed? Does the company utilize a broker?9.3.2Complete hedge documentation (if applicable) What information

15、 is captured? How is this information captured? Who maintains records? How is this information tracked?9.3.3Determine proper accounting treatment How does the company ensure compliance with GAAP? How do you monitor changes in GAAP requirements?9.3.4Calculate and record gains and losses on sale (if a

16、pplicable) Who is responsible for managing the sale of securities? Who approves the sale of securities? Who is responsible for calculating and recording the sale? Who calculates the gain or loss on sale? Who reviews? Is an approval needed to sale securities at a loss? Who records in the general ledg

17、er? How are the proceeds from sale received? 9.3.5Record related assets and liabilities Who has access to record? Who reviews? How is activity tracked? What reconciliations are performed?9.3.6Calculate and record periodic market valuation adjustments in accordance with applicable accounting standard

18、s Who has access to record? Who reviews? Who monitors compliance with applicable accounting standards?9.3.7Calculate and record settlements for related contracts. Who has access to record? Who reviews? How is activity tracked? What reconciliations are performed?Page 4 of 4April 2007DISCLAIMER: These questions are NOT all inclusive. This template is to be utilized as a starting point when conducting interviews with client process owners which may require additional follow up questions to capture the existing control environment.

- 温馨提示:

1: 本站所有资源如无特殊说明,都需要本地电脑安装OFFICE2007和PDF阅读器。图纸软件为CAD,CAXA,PROE,UG,SolidWorks等.压缩文件请下载最新的WinRAR软件解压。

2: 本站的文档不包含任何第三方提供的附件图纸等,如果需要附件,请联系上传者。文件的所有权益归上传用户所有。

3.本站RAR压缩包中若带图纸,网页内容里面会有图纸预览,若没有图纸预览就没有图纸。

4. 未经权益所有人同意不得将文件中的内容挪作商业或盈利用途。

5. 装配图网仅提供信息存储空间,仅对用户上传内容的表现方式做保护处理,对用户上传分享的文档内容本身不做任何修改或编辑,并不能对任何下载内容负责。

6. 下载文件中如有侵权或不适当内容,请与我们联系,我们立即纠正。

7. 本站不保证下载资源的准确性、安全性和完整性, 同时也不承担用户因使用这些下载资源对自己和他人造成任何形式的伤害或损失。